In what could prove to be a pivotal month, September saw a swath of central banks pause at what many hope will be the end of the historically swift monetary policy tightening cycle. The Federal Reserve led the pack (along with the BOE, RBA, SNB and many others) to put on hold, at least for now, further hikes in their policy rate. As usual it was all rather blandly stated in the official FOMC statement.

“The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. In support of these goals, the committee decided to maintain the target range for the federal funds rate at 5-1/4 to 5-1/2 percent.”

https://www.federalreserve.gov/newsevents/pressreleases/monetary20230920a.htm

Chair Powell provided significantly more colour in the subsequent press conference.

Despite stating that they “see the current stance of monetary policy as restrictive, putting downward pressure on economic activity, hiring, and inflation”, they raised their previous projections for GDP growth from the previously released Summary of Economic Projections (SEP). Much of the market commentary revolved around the premise that the Fed is now outlining a base case of a “soft-landing”.

https://www.federalreserve.gov/mediacenter/files/FOMCpresconf20230920.pdf

More interesting, from our perspective, was the speech given by Chair Powell a week later. Chair Powell joins the swelling ranks of central bankers stressing the importance of influencing the public’s behavior through their communication efforts.

“As many of you know, the Fed’s ability to influence the economy depends to some extent on influencing the public’s view of current and future economic conditions. When my colleagues and I publish our projections for the most likely path for the economy and interest rates, as we did a couple of weeks ago, one of our goals is to influence spending and investment decision today and in the months ahead.”

https://www.federalreserve.gov/newsevents/speech/powell20230928a.htm

This echoes many such comments previously from the central bank world’s glitterati that we have discussed in these pages.

In our February 2023 Update – “Sharpe World!™ is Nefarious”, we referenced a speech by outgoing BOJ Deputy Governor Wakatabe and quoted him thusly:

“The key to modern monetary policy is expectation management….Communication with the general public is particularly important since their perception plays a key role in anchoring inflation expectations, and thus, affect the actual evolution of inflation.”

https://convex-strategies.com/2023/03/16/risk-update-february-2023-sharpe-world-is-nefarious/

Then, again, in our June 2023 Update – “One Thing”, we reference the public comments of BOE Chief Economist Huw Pill at the ECB Sintra Conference.

“Then ultimately how you convert that into a way of communicating with the public and financial markets. Monetary policy, and indeed economic policy making more generally, can have an effect on behaviour which supports what you are trying to achieve and internalizing that benefit is one that is pretty key to having a framework that just doesn’t put accurate forecasts, in some abstract sense, on a pinnacle above the thing that is the real importance of what the underlying process is.”

https://convex-strategies.com/2023/07/13/risk-update-june-2023-one-thing/

And, again last month, we noted ECB President Lagarde’s speech explicitly on the topic of central bank communication efforts.

“Communication plays a crucial role in influencing people’s inflation expectations.”

One thing seems clear, there is plenty of communication going on between central bankers…and more than enough to send a shiver down one’s spine!

Fortunately, we are not all alone in our concerns about the, without any empirical support, self-declared omnipotence of central bankers. Our guru of financial history, and the editor of the eponymous Grant’s Interest Rate Observer, Jim Grant, gifted us with this recent public interview on CNBC.

The interview is chock-full of absolute pearls of wisdom. We suspect that Jim, like ourselves, quite seriously questions the Fed’s ability to foresee the future, much less to direct it.

“We have been used to, I think, imputing to the Fed immense powers of foresight and control. But oftentimes, the Fed, like so many of us, finds itself not in the vanguard of action or thought, but rather running behind to catch up.”

If we had a vote (clearly, we don’t!), we would cast it towards what one interviewer proposed as the “Grant Rule”:

“The rule would be that interest rates ought to be discovered in the market, rather than imposed or suppressed.”

Hallelujah!

We endlessly ponder the question as to why/how a trivially small group of people, with barely a sliver of a difference in world views and absolutely no skin-in-the-game, can decide they somehow know better than millions upon millions of explicitly accountable market participants what the price of borrowing and lending should be.

“Pretium iustum mathematicum, licet soli, Deo notum.”

We noted this Latin quote in our July 2022 Update – “The Pointlessness of Forecasting”.

“We led off this Update with a Latin quote. Hayek introduced us to the term in his aforementioned speech. He attributes it to “the Spanish schoolmen of the 16th century”; “pretium mathematicum, the mathematical price, depended on so many particular circumstances that it could never be known by man but was known only to God.”

Going back to Jim’s interview, he makes the early point referencing the Chicago Fed’s Financial Conditions Index. A quick graph very clearly shows the point that he was making.

Figure 1: Chicago Fed National Financial Conditions Index (white) and US Tsy 10yr Yield (blue)

Source: Bloomberg, Convex Strategies

You can see that in recent months, say since March 2023 when the Silicon Valley Bank and Credit Suisse issues transpired, the Financial Conditions Index has consistently declined, indicating looser conditions. This despite the fact that 10yr Treasury yields have continued to rise.

To Jim’s point, contrary to Chair Powell’s statement we quoted above of policy now being “restrictive”, this would seem to indicate potentially otherwise.

Interestingly, we note that back in the heady inflation years of the late ‘70s and early ‘80s, the Financial Conditions Index was above even the peaks of the recent cycle for more than 6 continuous years. Are we to accept Chair Powell’s “restrictive” conclusion?

Another interesting tidbit we thought worth adding to the above picture, and we think relevant to Jim’s subsequent comments, is the evolution of the US Federal Debt/GDP over this same period.

Figure 2: Chicago Fed National Financial Conditions Index (white). US Tsy 10yr Yield (blue). US Federal Debt/GDP (red)

Source: Bloomberg, Convex Strategies

The Debt/GDP line is certainly one of those things that makes one want to say maybe “this time is different”. When last brave central bankers tightened financial conditions and pushed 10yr yields to 14% and beyond (as Jim mentions), the US Federal Debt/GDP was hovering around 30%. That is a far cry from today’s circa 125%. It would be possible to make an argument that the system is somewhat more fragile today.

We have opined for a good long time, using our catch phrase of “who’s going to own the 40?” (the notional allocation to fixed income in a 60/40 portfolio), that the ultimate pain for the market, given the mass of ludicrously low yields on government debt and the historically extreme size of debt issued (Jim notes the historical madness of negative nominal yields), that the ultimate pain for the market would be the dreaded bear steepening of yield curves. The pain, in any undesired market environment, always comes from the same thing: too much leverage, aka undercapitalized risks.

As both nominal rates were lowered down to and through 0% and as Debt/GDP ratios exploded from deemed stable levels through the previously considered unallowable 100% threshold, ever more accommodative regulatory risk and accounting constructs were put in place to absorb the debt into financial intermediaries. The sovereign debt, as we have often observed, in the regulated realm and supported by academia, existed on a spectrum between riskless and risk reducing. What we call Sharpe World.

As back-end rates rise, the continuing lack of loss absorbing capital assigned to those risks just keeps hurting and hurting. We obviously don’t know what was in the minds of the FOMC members (nor any other central bankers) when they decided to ‘pause’ in September, but we would suspect it wasn’t that they were going to trigger a furtherance of global bear steepening in rate markets.

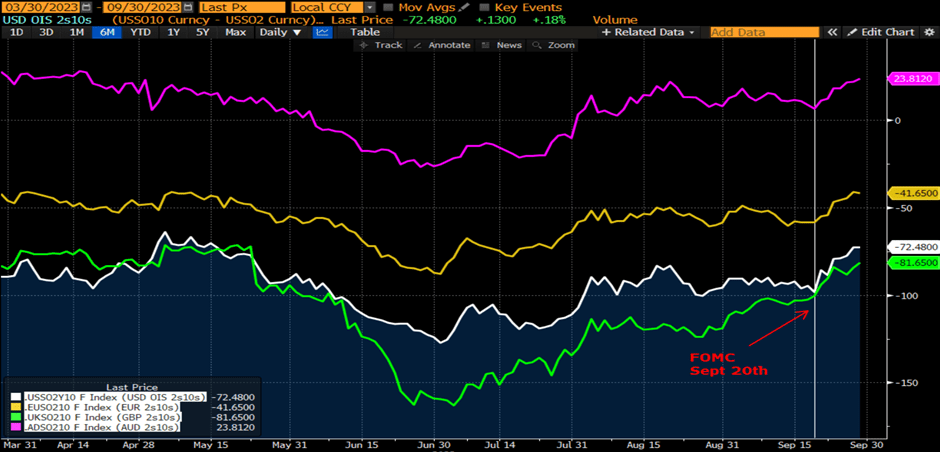

Figure 3: 10yr Swap – 2yr Swap USD (white), EUR (yellow), GBP (green), AUD (purple). FOMC Sept. 20th Meeting (vertical)

Source: Bloomberg, Convex Strategies

Just dragging the start date back for some perspective on where we have come from.

Figure 4: 10yr Swap – 2yr Swap USD (white), EUR (yellow), GBP (green), AUD (purple). FOMC Sept. 20th Meeting 2023 (vertical)

Source: Bloomberg, Convex Strategies

We have long been of the opinion that central bankers would be best served by keeping the curves inverted, limiting the pain of unrecognized duration losses on the Sharpe World entities holding all their bonds, until they got to the recession that they seem to desire and, thus, limit any curve steepening to the far more common bull steepening dynamic. In other words, get to the recession so the market would willingly continue to buy and hold the bonds. A failure to vanquish the inflation beast, thus risking yet further deterioration of monetary and fiscal credibility, brings us back to the unmanageable dilemma of nobody wanting to own the “40”. A circumstance that may be indicative of a fairly reflexive relationship with the dreaded bear steepener. As the below scattergram of the historical occurrences of bear/bull flattenings/steepenings indicates, maybe the good news is that bear steepenings just don’t happen. On the other hand, that may entail a certain lack of capitalized risk in a world that uses frequencies within historical lookbacks as a flawed projection of probabilistic future risk, not to mention stochastic processes in longer dated path dependent option hedging models.

Figure 5: Top 100 30d changes in US 10y-2y curve vs changes in 10y and 2y US Tsy Yields (1976-2023)

Source: Bloomberg, Convex Strategies

It is still early to make definitive observations, but probably safe to say that the ‘pause’ has, thus far, not gotten off to a good start, at least as defined by stability of long duration interest rates. Take the EUR 30yr swap rate as an example of something that, at least visually, could be termed as concerning.

Figure 6: EUR 30y Swap Rate

Source: Bloomberg, Convex Strategies

Back to our point regarding their own presumed importance around communication to influence the expectations and behaviour of ordinary consumers, the ECB has a particularly daunting task. President Lagarde and her troop of behavioural influencers need to get economic participants across a vast array of circumstances such that some lean a little bit to the left while others lean a little bit to the right as they try to precisely fix one interest rate (presumably targeted at just the right mythical ‘neutral rate’) to influence inflation expectations across a broadly dispersed range of actual realized price changes. Hopefully the ECB communication comes with a range of specific “taylorizations”.

Figure 7: Core HICP YoY% Germany (white), Italy (papaya), Austria (purple), Slovenia (yellow), Lithuania (fuscia). ECB Deposit Rate (blue)

Source: Bloomberg

Meanwhile, over on our side of the world, the 2nd and 3rd largest economies in the world, China and Japan, continue to run with extraordinary market manipulation, day in and day out.

China continues to apply maximum CCF (Countercyclical Factor) adjustments to their daily fixing, preventing the weakening of the CNY that, as we said above, millions of market participants would apply in their free and voluntary transactions.

Figure 8: PBOC Fixing Bias. Bloomberg Fix Estimate (FCCNYFIX Index) minus PBOC Midrate (CNYMUSD Index)

Source: Bloomberg, Convex Strategies

We don’t know for sure, but one could surmise that the pressure on the currency and the commitment from the PBOC to hold it steady, could be related to an ever-declining amount of US Treasury holdings by China. Maybe they aren’t going to own the “40” either.

Figure 9: US Treasury Holdings by China per monthly TIC data

Source: Bloomberg

Then, just across the East China Sea, we have Japan who continue with their historically extreme accommodative policies. Once again, they are on track to buy up JGBs this year at a pace roughly on par with last year’s circa $1trillion worth of bond purchases. Contrary to what the BOJ keeps assuring us, by our measures of CPI exFresh Food and Energy and $/JPY levels, it seems to be working.

Figure 10: Japan CPI exFresh Food and Energy (white). USD/JPY (papaya). JGB 2yr Yield (blue)

Source: Bloomberg

We are well past our Q1 2022 outlier of “working” at 4% and $/Yen 145. By the next BOJ meeting, October 31st, we could be in sniffing distance of our revised level of 5% and $/Yen 155. When will the BOJ start to wonder if their policies are working?

We might get a hint at the October meeting when they release their latest revised projections. Just a little reminder of what their current projection for FY’23 implies for the confidence in their reflationary policies.

Figure 11: Japan CPI ex-Fresh Food and Energy (white) and Estimated Future Path to Achieve BOJ Forecast (multi-coloured)

Source: Bloomberg, Convex Strategies

October ought to be interesting.

Read our Disclaimer by clicking here