Ever lower interest rates is the answer. Nobody seems to know, or care, what the question is.

Both the Federal Reserve and the ECB dialled up their monetary easing in the month of September with rate cuts and renewed balance sheet expansion, with seemingly little concern for the success of such policies to this point. Whatever it is / was that they hoped to achieve from years of unprecedented monetary extremes, they apparently have yet to achieve it. Their only answer is simply more of the same.

We have discussed before the concept of the “Reversal Rate”. The concept that ever more accommodative monetary policy eventually becomes counterproductive and becomes contractionary. This concept, not surprisingly, was first actively discussed within and by the Bank of Japan, and represented in a number of research pieces such as:

https://www.imes.boj.or.jp/research/papers/english/19-E-06.pdf.

Our friends at the BIS have also done some work recently on what is, more or less, the same concept:

https://www.bis.org/publ/work807.pdf.

Both of these papers are quality mathematical / Keynesian / model studies of what could be termed “common sense”. If interest rates get pushed sufficiently low, there is an obvious negative impact on the profitability of banks. In particular, if you reduce the profitability of lending, you might find that banks are less likely to lend, or at the very least have less accumulated capital to lend against.

We’ve been showing the Japan version of the following charts for decades, but it still holds up pretty darn well. This is simply Japanese bank equity prices versus JGB 10yr yields.

Source: Bloomberg

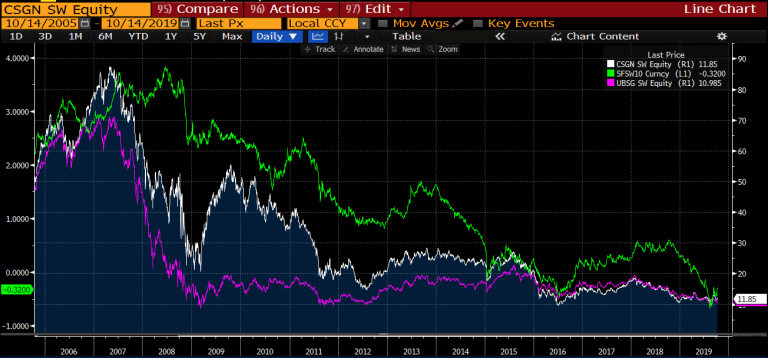

Not overly surprising, since going to ZIRP and QE, we see quite similar outcomes in the Eurozone, Switzerland, and the UK.

Source: Bloomberg

Source: Bloomberg

Source: Bloomberg

Of course, in the case of the ECB, the term of “Mr Whatever it Takes” Mario Draghi is now up and he is being replaced by Christine Lagarde, (in)famous for her past roles as Head of the IMF and as France’s Finance Minister. Ms Lagarde made comments recently with regards to the extreme monetary policy du jour and negative interest rates, saying “we see the recent introduction of negative interest rates by the ECB and Bank of Japan – though not without side effects that warrant vigilance – as net positives in current circumstances”. We plead for her to produce something indicative of even gross positives, much less net. If you think that the powers-that-be aren’t willing to overlook the practical implications of NIRP (ie. penalize wage earners for saving) and would just plough down the road of dystopian technicalities into the land of model madness, then you should have a good read of this little peach of research under the umbrella of the IMF:

https://www.imf.org/en/Publications/WP/Issues/2019/04/29/Enabling-Deep-Negative-Rates-A-Guide-46598

The simple question for our Central Banking overlords is can you stimulate economies while destroying the industries that exist to intermediate savings? In other words what are the unintended consequences on banking, pensions, insurance, etc? Is more of what got us to this point likely to result in something different down the road?

It isn’t too hard to find a couple of prominent standout exceptions to the convergence of bank equity values and interest rates to zero. There again, these two countries are just about the only guys left with a modicum of nominal interest rates; USA and Australia.

Source: Bloomberg

Source: Bloomberg

In recent months, we have seen revised interest rate cuts by both the Fed and the RBA, two of the few remaining central banks with positive rates and thereby some capacity to cut further.

Source: Bloomberg

Will these two policy makers continue to cut rates? Will they “go to zero”? Will they go negative? If they are paying attention to what has happened to the banking markets of their already zero / negative brethren, you would hope that they would err on the side of caution. Nevertheless, most rhetoric and research seems to indicate that they are very willing to go there, maybe even guiding the market to prepare for such an outcome.

Presumably, the extraordinary policy settings are intended to deal with extremes in their macro-policy objectives, namely growth and inflation. Yet it is hard to really see that these macro conditions are themselves at some sort of historical extreme.

Source: Bloomberg

Cynical folks tend to suspect that the extraordinary monetary policy might have something to do with supporting asset prices. When you normalize GDP, CPI and the S&P Index, it certainly gives some impression that the long term volatility of economic growth and consumer prices truly pale in comparison to equity prices. It certainly looks suspicious that there may be a link between extreme monetary policy and asset prices, maybe particularly financial asset prices.

Source: Bloomberg

This is of course what leads to the oft-cited claim that ZIRP/NIRP/QE are the principal drivers of wealth segregation, which in turn has been attributed with linkage to the socio-political instability the world over. It certainly seems feasible that the policy makers could be striving for their desired “growth” through the wealth effect on consumption. We are more than just suspicious of this, as we have heard as much straight from the lips of no less than Alan Greenspan himself.

To wrap up, it isn’t too difficult to make an argument that extreme monetary policy has done more harm than good. Even as central banks have shown they can violate the zero-bound, they too seem cognizant that there are problems with going too far into negative territory. What is the efficacy to continue holding large tracts of Fixed Income as a supposed risk mitigant in a long term “balanced” portfolio? If it is asset prices that they are trying to inflate, then own assets! And own some highly effective protection just in case they get it wrong.

Source: Bloomberg

Source: Bloomberg

Read our Disclaimer by clicking here